WHAT THIS ARTICLE IS — In three years, India’s most valuable startup went from $22 billion to zero. This is not a story about bad luck. It is a step-by-step account of how governance failure, unchecked acquisitions, and dollar-denominated debt destroyed a company that hundreds of millions of students depended on — and the four lessons every founder building today must take from it before it is too late.

BENGALURU — In October 2024, Byju Raveendran sat before a camera and said three words that no founder in the history of Indian startups had ever said about their own company: “the company is worth zero.” It was not a metaphor. It was a fact. The edtech giant that had once been valued at $22 billion, making it India’s most valuable start-up, had collapsed to effectively nothing. The fall from peak to zero took less than three years.

The Byju’s story is not simply the story of a company that failed. It is a systematic case study in what happens when growth becomes a substitute for governance, when ambition outpaces accountability, and when the signals of approaching collapse are ignored or denied at every stage. For Indian founders building today, it is the most instructive collapse in the ecosystem’s short history.

Byju Raveendran on stage at the height of Byju’s rise — a $22 billion valuation, 50,000 employees, and 150 million registered students. The fall to zero took less than three years.

HOW BIG IT GOT — AND HOW FAST

Founded in 2011 by Byju Raveendran, a teacher from Kerala who turned a knack for coaching students into a digital learning platform, Byju’s raised over $5 billion from marquee global investors including Sequoia Capital, Tencent, Prosus, Tiger Global, and the Chan Zuckerberg Initiative. At its peak in 2022, it employed over 50,000 people and claimed 150 million registered students worldwide. FY22 gross revenue was reported at nearly ₹10,000 crore.

The pandemic accelerated everything. Locked-down students across India turned to digital learning in large numbers, and Byju’s was the primary beneficiary. Valuations soared, investor cheques multiplied, and the company expanded at a pace that in retrospect was entirely free from its operational capacity to absorb that growth.

THE ACQUISITION SPIRAL

Between 2019 and 2021, Byju’s went on one of the most aggressive acquisition sprees in Indian startup history. It acquired Osmo for $120 million in 2019, WhiteHat Jr for $300 million in 2020, and then, in 2021, spent close to $2.5 billion on nine acquisitions in a single year. Among them: Aakash Institute for approximately $1 billion, the US-based Epic for $500 million, Tynker for $200 million, and Great Learning. The total acquisition bill across this period exceeded $2.5 billion.

None of these were cheap deals. Many were done at premium prices, funded by a combination of equity and debt. The company had raised $1.2 billion through an overseas term loan in 2021, a decision that Raveendran would later call their biggest mistake. Integration was poor. Synergies did not materialise. Cash began to drain. And the acquisitions, rather than becoming engines of growth, became liabilities that compounded the central problem: Byju’s was spending at a rate its revenue could not justify.

GOVERNANCE FAILURE IN STAGES

What makes Byju’s particularly instructive is how visibly governance eroded, stage by stage, in full public view. In June 2023, Deloitte resigned as the company’s auditor, citing repeated delays in financial reporting and a lack of cooperation. Simultaneously, three key board members representing Sequoia (now Peak XV), Prosus, and the Chan Zuckerberg Initiative also walked out. The company that had once had global institutional oversight was now left with Byju Raveendran, his wife, and his brother as its only directors.

The National Company Law Tribunal, where Byju’s insolvency proceedings played out in 2024. Claims worth over $1.5 billion were filed by 1,887 creditors.

The audit delays had triggered a technical default on the $1.2 billion term loan. Lenders came for their money. In June 2023, Byju’s skipped a $40 million interest payment, making it one of the largest Indian startups ever to miss a dollar loan payment. It then counter-sued its own lenders. $533 million from the loan was alleged by creditors to have been transferred into a hedge fund, with no clear explanation from management.

Tax authorities piled on. Reuters reported in September 2024 that Indian tax authorities sought nearly $101 million in dues from the company. The BCCI dragged it to court over ₹158 crore in unpaid sponsorship dues. By July 2024, the National Company Law Tribunal had appointed an Insolvency Resolution Professional to oversee Byju’s day-to-day operations. Claims worth over $1.5 billion had been filed by 1,887 creditors.

The US assets fared no better. Epic, acquired for $500 million, was eventually sold to China’s TAL Education Group for $95 million. Tynker, bought for $200 million, was sold for just $2.2 million. In May 2026, a Singapore court sentenced Raveendran to six months in jail for contempt of court linked to disclosure obligations.

WHAT EVERY FOUNDER MUST TAKE FROM THIS

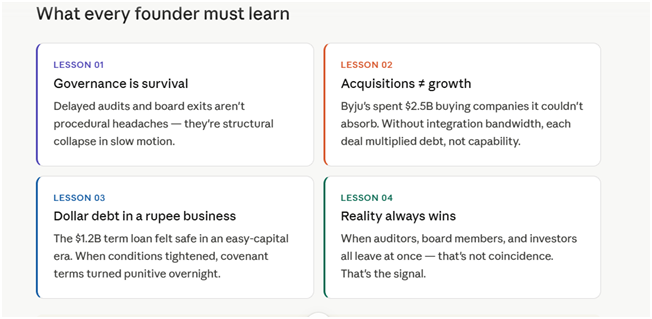

The Byju’s collapse distils into four hard lessons. The first is that governance is not bureaucracy — it is survival infrastructure. Delayed audits, opaque financials, and the departure of independent board members are not procedural inconveniences. They are early warnings that a company is losing the structural integrity required to function at scale.

The second is that acquisitions are not a growth strategy. Buying companies at premium prices, without the operational bandwidth to integrate them, does not add capability. It multiplies complexity and debt. Byju’s spent over $2.5 billion acquiring businesses it could not absorb.

The third is about the specific danger of dollar-denominated debt for rupee-revenue businesses. The $1.2 billion term loan was raised in a period of abundant global capital, at a moment when Byju’s valuation made lenders comfortable. When conditions changed, the covenant structure turned punitive instantly. Founders taking on foreign-currency debt without stress-testing their ability to service it in a tighter capital environment are carrying a risk that may not be visible until it is too late.

The fourth, and perhaps the most difficult, is about the relationship between a founder and reality. The people closest to the truth at Byju’s — auditors, board members, investors — left when they could no longer reconcile what they were being told with what they were seeing. When every institutional check walks out at the same time, the signal is unambiguous.

India’s startup ecosystem has produced extraordinary companies. It has also now produced its most cautionary tale. The Byju’s collapse is not a story about one bad actor or one bad decision. It is a story about a system — of capital, of governance, of founder ego that failed to self-correct until the damage was irreversible. The founders building today have no excuse not to have read it.

{kind=link}